A company like SpacePharma, supplier of automated testing procedures in space, has a very favorable point of departure: they have found an extremely innovative topic – without competition thus far – and have a unique product for which there is currently no market but a need. Backed with sufficient financing, they can further develop and implement their ideas for years. But market segments that are already developed can also be targeted successfully. This article takes a look at current conditions on the German market and provides useful tips for successful market entry.

Worthwhile sectors for investment on the German healthcare market

Germany, the world’s fourth-largest industrialized economy, spends EUR 4,213 per inhabitant on health. With a volume of EUR 344.2 billion, the German healthcare market is very attractive for companies from all over the world. High-quality medical equipment with a good price-performance ratio that keeps up with the trends in computerization, molecularization and miniaturization has the best prospects here:

- Besides the convergence of medical technology and information technologies, computerization includes the development of high-performance implants through improved hardware and software, model-based image processing, and the intelligent control of dialysis and ventilation systems.

- Molecularization includes, inter alia, nanoparticles that release drugs in a controlled fashion and the development of new functional biomaterials that imitate natural tissues.

- Devices meet the miniaturization trend that, for instance, enable an examination directly at the doctor’s office and the application of implantable micro-systems that work sensorially, by telemetry, or with a connection to nerves.

Other areas also promise high potential for suppliers from Germany and abroad. These include these fields of research into which most investment in Germany is currently going1:

- Imaging techniques, such as 3D imaging combined with navigation and representation of instruments or hybrid imaging procedures

- Prostheses and implants, like prostheses with sensors, actuators and control loops, fall detectors or biofunctional implants

- Telemedicine and model-based therapy, such as process optimization by deploying IT, Critical Incident Reporting Systems (CIRS) or

- Clinical Decision Support Systems

- Operational and interventional devices and systems, like the connection between instrument and data record, augmented reality or combined methods (endoscopy with imaging)

- In-vitro diagnostics (IVD), such as POC diagnostics with lab-on-a-chip systems or multi-array systems for complete analyses with small sample quantities

- Technology for “regenerative medicine”, such as artificial tissue models.

Specific features of the German healthcare market

The challenges on the German market are above all in competition, in reimbursement and with customers. The German market is widely distributed; relationships between suppliers and care providers are strong – meaning that even a company with a product with a persuasive USP has to face up to the competition.

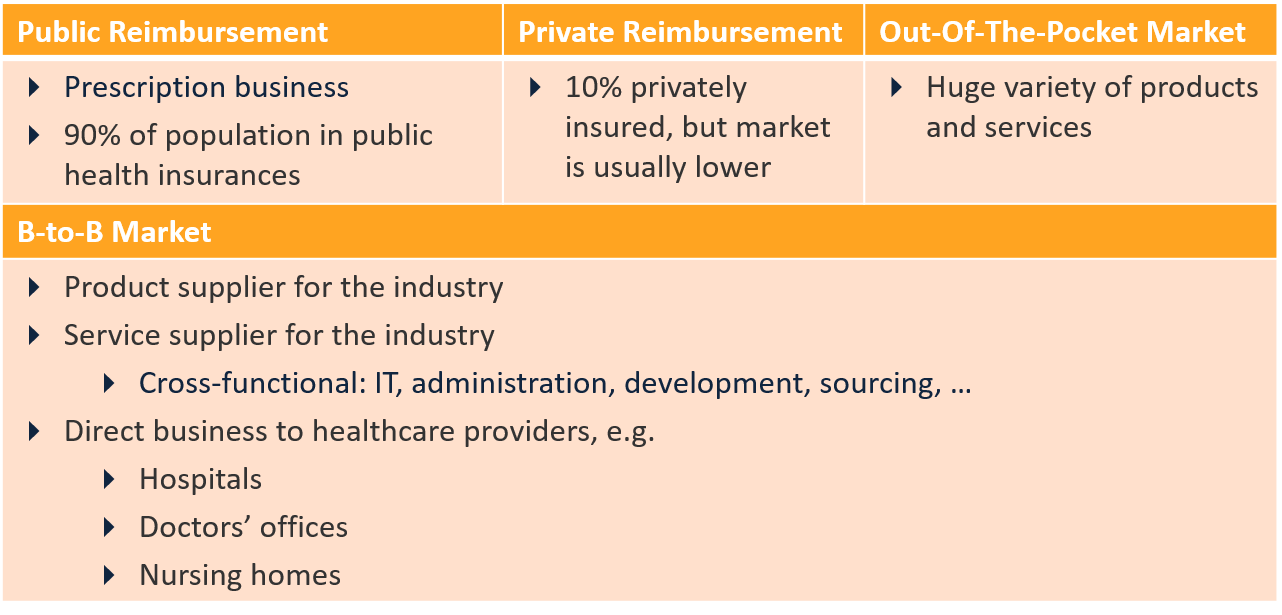

About 58 percent of the market is financed by statutory health insurers; an additional 8.9 percent comes from private health insurers. The requirements from reimbursement are thus clearly defined. The German Technical Aids Register serves as the “gatekeeper” for reimbursement in outpatient care. Often, the new product does not match the product groups, and for that reason alternative sales channels must be developed.

In B2B business, the focus is on hospitals, doctors’ offices and pharmacies. Business with hospitals is complex since the decision-making processes – particularly for capital goods – vary greatly. A survey of 404 hospitals2 identified twelve different decision-making bodies: from the chief physician to the managing director to the IT, medical technology or purchasing department – and various combinations thereof. In addition, doctors’ offices are difficult to reach with a dispersed sales force.

The challenges – taking mobile apps and e-health solutions as an example

A large share of the companies that want to capture the German market come from the booming segment of mobile applications. Successes here are few and far between, as there is often a lack of business models3. Only a few approaches are promising for medical apps in Germany. One possibility is financing by statutory and/or private health insurers or the sale of the application to the end users. Selling to existing care providers is another option. Thus, for instance, providers of emergency call services are a sought-after target group for providers of monitoring apps (wearables).

Apart from the question about the business model, suppliers of mobile applications and those of other e-health solutions should have answers to questions that are crucial for success:

- What existing (medical care) process is improved by means of the application?

- What are the advantages for users in everyday use (e.g., real time savings)?

- How significant are the changes for users?

- How much effort must be expended for IT administration, data or decision management?

Many applications on the market reveal an alarming lack of knowledge about real medical care processes in hospitals, doctors’ offices or at home.

Step-by-step support for market entry

The decision on which market segment to position one’s product helps define the guiding principles for going forward, particularly what path one embarks on to the source of money. On the market for statutory health insurers, these guiding principles are the obstacles to reimbursement, while on the market for privately insured individuals it is customers’ own budgets.

The challenges, not just in the B2B segment, are in driving out the existing relationships between manufacturers and customers. Besides in marketing and sales, there are also often care concepts that have to be implemented together with the care providers, such as pharmacies or medical supply stores.

Figure 1: Market segments for positioning

For each step, you need competent support from the market – and that’s what the Healthcare Shapers offer: the network can provide experienced experts with the appropriate knowledge from development, approvals (medical technology), to market access with topics like reimbursement, market know-how, sales concepts and care models, to implementation.

Sources:

1 Aachener Kompetenzzentrum Medizintechnik – AKM und AGIT mbH; Zur Situation der Medizintechnik in Deutschland im internationalen Vergleich [On the Situation of Medical Technology in Germany in an International Comparison], Feb. 4, 2005.

2 FAQ Consulting GmbH, survey of 404 German hospitals, 2011, for results ask the author.

3 mHealth App Market Sizing 2015 – 2020, Research2Guidance.

Autoren des Beitrags